--Growth and Segmentation of the Chinese Low-Voltage Electrical Appliances Market

Driven by the "dual carbon" strategy and the construction of the new power system, China's low-voltage electrical appliance industry is experiencing a historic opportunity for development. As a key basic equipment in the power system, the low-voltage electrical appliance industry is accelerating its transformation and upgrading towards intelligence, greenness and internationalization, demonstrating strong development momentum and broad market prospects.

The growth and segmentation of the domestic low-voltage electrical appliances market in China

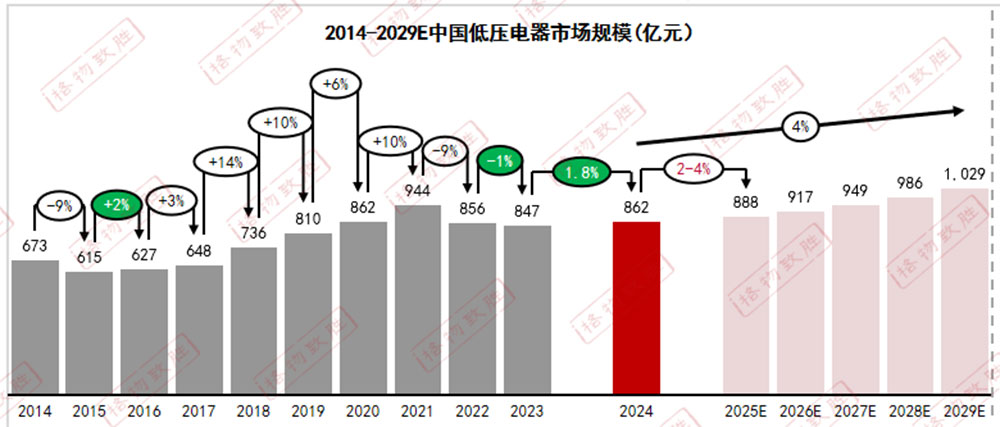

01 The overall market size

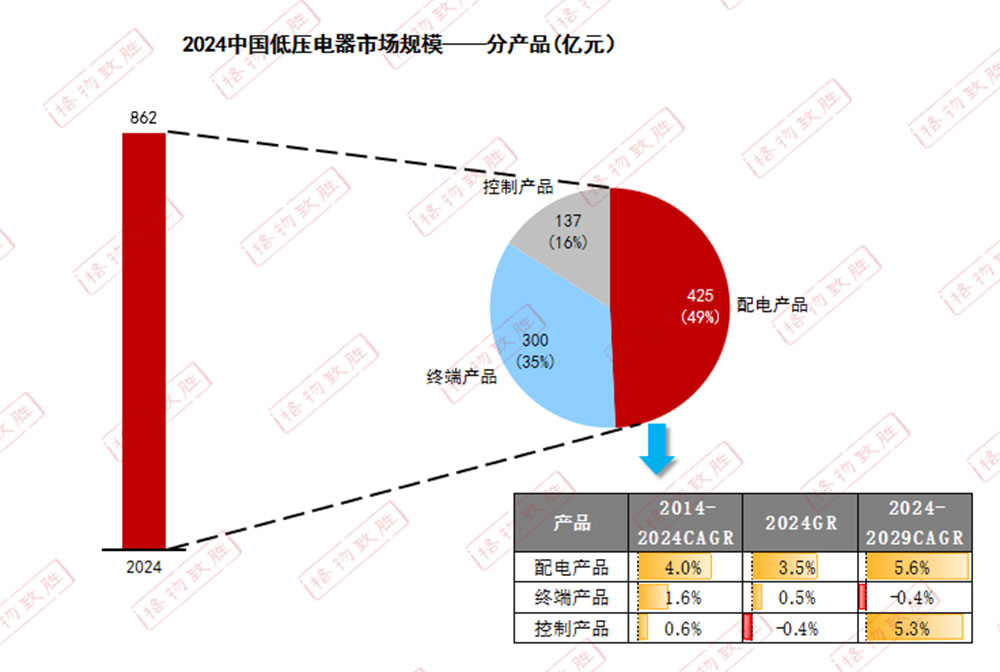

02 Segmented products

The market share of power distribution equipment is close to half, and it is expected to have the best growth rate in the future.

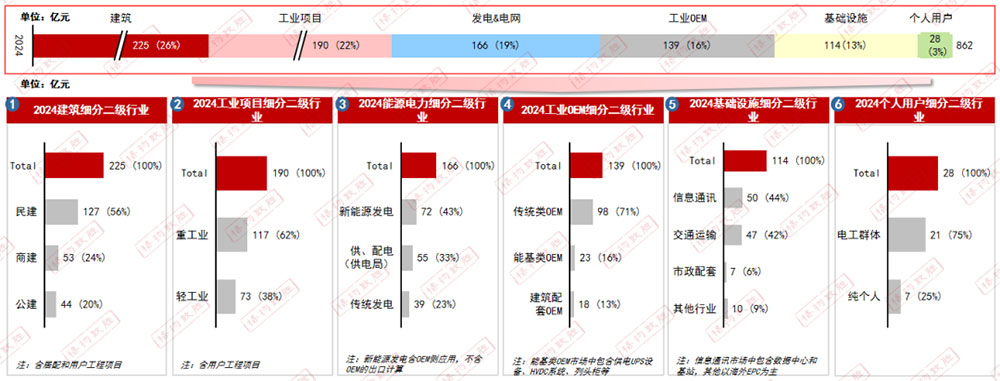

03 Subdivision of primary and secondary industries

Low-voltage electrical appliances are mainly applied in the construction and industrial sectors, accounting for approximately 48% of the total, with the proportion showing a downward trend. Among the sub-sectors, those with a larger proportion in the construction industry include residential buildings and office buildings; in the industrial sector, the ones with a larger proportion are chemical, metallurgical, petrochemical & oil industries, and the food and beverage industry in the light industry also has a significant share.

04 Sub-sectors

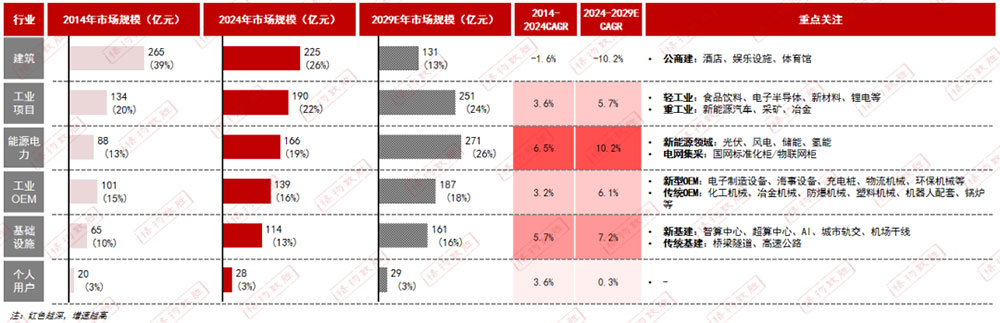

The largest application sector accounted for nearly 40% in 2014. As the real estate bubble burst, its share began to decline, and it is expected to continue to show a significant downward trend in the future.

The market size is steadily increasing. With the accelerated layout of "new quality productive forces" and the gradual release of demand for equipment renewal and renovation, there will be considerable market potential in the future.

The industry with the best growth rate is mainly driven by new energy projects and grid investment;

The growth rate of the OEM industry related to construction has fallen short of expectations. However, the performance of new fields such as logistics machinery, consumer electronics, semiconductor equipment, maritime equipment, and industrial smelting furnaces has been relatively better.

The supercomputing and artificial intelligence computing in data centers, as well as the overseas market, have witnessed explosive growth, which has significantly contributed to the steady expansion of the overall industry's market size.

05 Segmented sales strategy

2024 China Domestic Low-Voltage Electrical Appliance Market Segmentation Sales Strategy

In 2024, low-voltage electrical products will mainly be applied in the channel market, accounting for 55%. Given the large number of participants in the channel market, the market competition is extremely intense, and it shows a relatively sluggish growth rate.

The market share in this industry is relatively small. Thanks to the favorable development trends in infrastructure and industrial markets such as data centers, electronics, ships, chemicals, and steel, the performance has shown a relatively optimistic development trend.

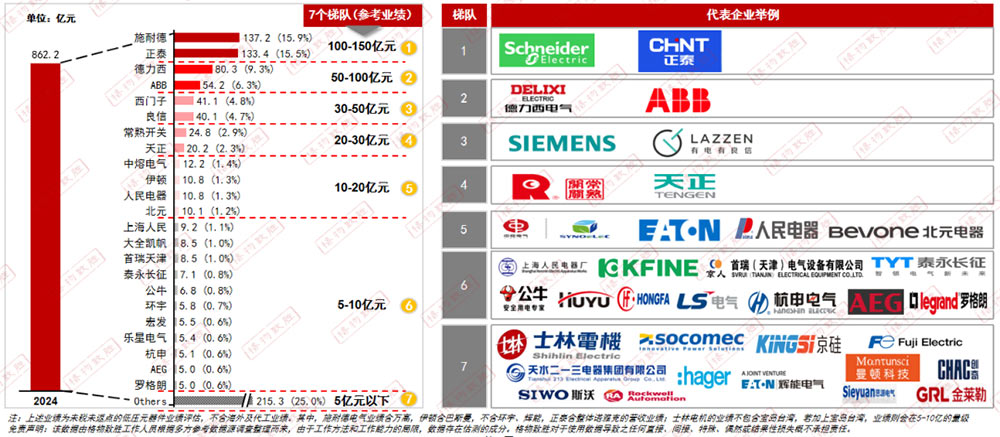

The competitive landscape and changes within the Chinese domestic market

2024 Domestic Competitive Landscape of Low-Voltage Electrical Appliances in China

Note: The above figures represent the assessment of the low-voltage component business without tax and without rebates, excluding overseas and OEM business results. Among them, Schneider Electric's performance includes Wan Gao, Eaton's includes Basmann, excluding Huan Yu and Hui Neng. Zhen Tai includes the revenue performance of the entire Noyacke; Shilin Electric's performance does not include Taiwan Province of China. If Taiwan Province of China is included, the performance will be at the level of 5-10 billion.

Shourui Tianjin (formerly Beijing Renmin, now Jingren brand)

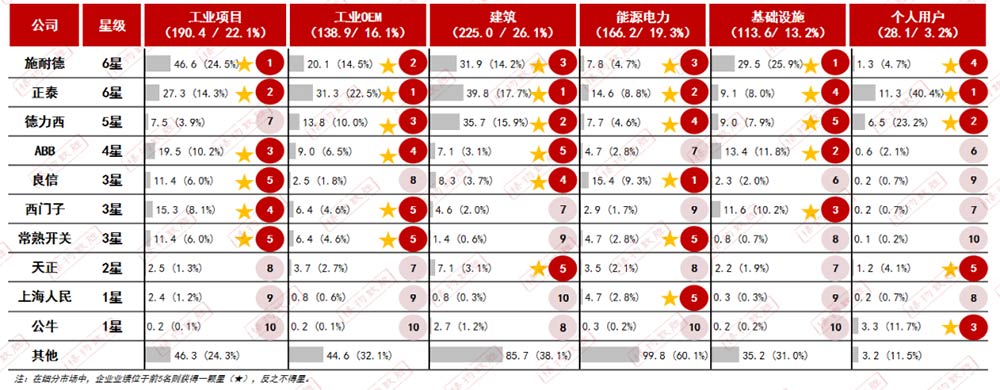

The market share of low-voltage electrical appliances in China

User Industry - 2024 (6-Star Market Model)

The domestic market share of low-voltage electrical appliances in China is analyzed using the "6-star market model". It mainly covers six user industries: industrial projects (22.1%), industrial OEM (16.1%), construction (26.1%), energy and power (19.3%), infrastructure (13.2%), and individual users (3.2%). The market shows a clear feature of concentrated leadership. Schneider (6-star) holds a leading position in industrial projects and infrastructure; ZTE (6-star) has the highest market share in construction and individual users; Delixi (5-star) performs outstandingly in the construction market.

Disclaimer: This data has been compiled by Xucky Electric staff based on multiple reference data sources. Due to the limitations of working methods and capabilities, the data contains elements of estimation. XUCKY assumes no responsibility for any direct, indirect, special, incidental or consequential losses resulting from the use of this data.